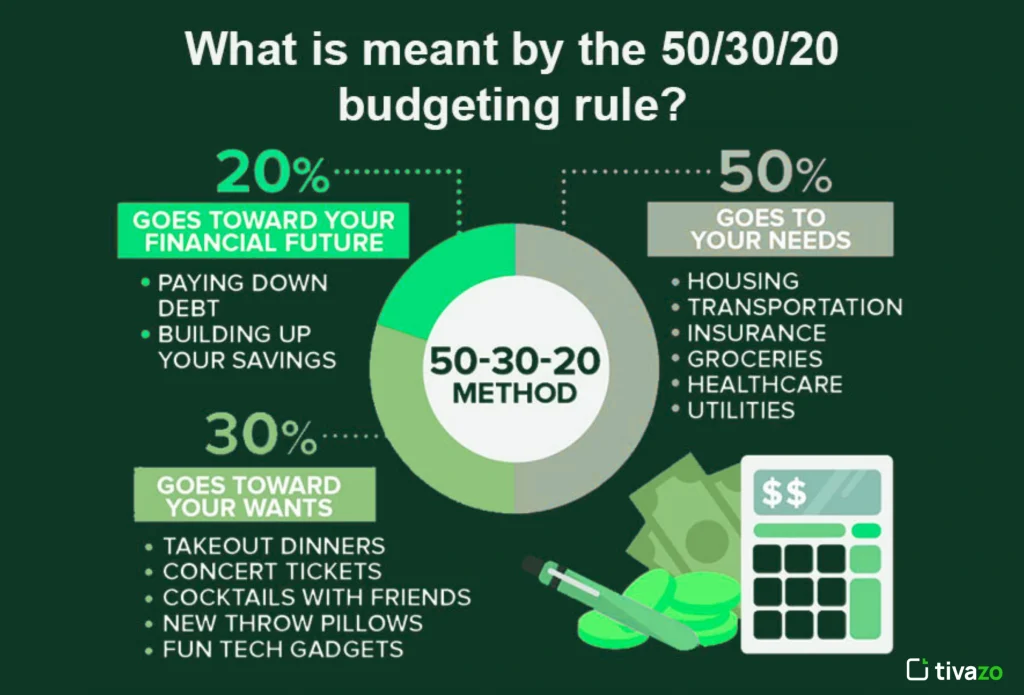

In individual financial management, the 50-30-20 Rule simply happens to be one of the simplest and most useful budgeting aids. It divides your after-tax earnings into broad categories: 50% for needs, 30% for discretionary spending, and 20% for saving or debt repayment. If you are a budget newbie or just plain want a tidier way to manage money, the rule offers an easy path to fiscal solvency.

Budgeting is more than noticing what you’re spending—paying attention, that is—it’s actually a practical means of achieving financial freedom, less stress, and securing tomorrow. In using the 50-30-20 Rule, you’re creating a system in which you’re taking care of needs first but still living today and investing in tomorrow. It is ideal for you as a single individual, couple, or even a family who wants to keep your finances without over-complicating the process.

As we embark on the 50-30-20 Rule in greater depth, you will learn how to apply it to your life, adjust it to your pay scale, and prevent budget traps. Ready to get started on managing your financial wellness? Let’s start

Unpacking the 50-30-20 Budget

The 50-30-20 Rule’s simplicity is its charm. By dividing your after-tax income into three groups only—needs, wants, and savings or debt repayment—you have a general sense of where your money has to go every month. This is how each group works:

🔵 50% Needs: The necessities of life

Half of your take-home pay should go towards necessities, the not-at-all-negotiable expenses that are required for your survival and well-being. These generally are:

- Rent or house payment

- Utilities (electricity, water, gas, etc.)

- Food and household essentials

- Transportation (car loan, gasoline, mass transit)

- Insurance premiums

- Minimum payments on debts

These are the ones you do not cut back on so readily, and if you’re above 50% of your after-tax income here, you’ll be forced to cut back on lifestyle or have cuts in fixed costs.

🟠30% Wants: Live It Up Within Limits

This is the most indulgent half of the 50-30-20 Rule—the 30% for wants. These are the items that make your life more comfortable but are not necessarily necessary. Refer to them as your indulgences and luxuries:

- Eating out and takeout

- Streaming services

- Shopping and clothing

- Vacation and travel

- Games and hobbies

Be truthful to yourself—sometimes we rationalize wants as needs. That weekend getaway or new phone launch may be alluring, but make sure they fall within your 30% budget.

🟢20% Debt Repayment and Savings: Invest in Your Future

Dedicate the final 20% to savings and debt repayment beyond the minimums. This is where financial stability and growth are really realized. Utilize this budget category for:

- Emergency deposits

- Retirement savings (IRA, 401(k), etc.)

- Additional credit card or loan payments

- Investments

- Savings for long-term goals (home, education, business)

This is the portion of the 50-30-20 Rule that prevents you from living check-to-check and actually building wealth and paying off future financial obligations.

To make the 20% work harder, park your emergency fund in a high-yield savings account. Competitive APYs, some as high as 5.00%, when you meet qualifying criteria, let your cash stay liquid while earning more, helping you grow your emergency fund faster. Automate transfers on payday and keep the fund separate from checking to avoid dipping into it.

Why the 50-30-20 Rule Succeeds?

The 50-30-20 Rule has become so an easy and popular budgeting method for a reason. Dividing how you spend your income into easy-to-grasp categories makes budgeting easy and accessible to anyone from any level of finance. Here’s why the 50-30-20 budgeting rule is so successful:

Simplifies Budgeting Process

The 50-30-20 Rule simplifies budgeting by applying only three categories. Instead of tracking each and every expense, you split your after-tax money into three general buckets: needs, wants, and savings/debt repayment. It’s simpler to make solid financial decisions without being overwhelmed by too much detail. It’s a quickie anyone can utilize, even beginners to budgeting.

Key Benefits:

- Easy and simple categories: You don’t have to classify every small purchase; simply watch the three large ones.

- Easy to obey: Without any intricate formulas or computer programs, the rule is easy for anyone to obey.

- Easy to monitor: At any given time, you can easily know how well you are sticking to your budget by checking the balance of your three categories.

Encourages Responsible Spending

One of the challenges in personal finance is resisting impulsive buys and being self-disciplined. The 50-30-20 Rule is a guide towards responsible spending through the setting of clear limits in all areas of the budget. Adhering to the rule ensures you first meet savings and essentials before giving in to desires.

Major Advantages:

- Promotes consciousness: You pay more attention to money spent and can easily recognize where you’re overspending.

- Reduces debt: By allocating 20% of your income to debt repayment and savings, the rule keeps you from getting buried in debt.

- Prevents inflation of lifestyle: With rising incomes, the rule compels you to save more instead of expanding your wants category.

Is flexible at various income levels

The 50-30-20 Rule is not a one-size-fits-all rule—it’s an elastic structure that adapts to your income. Whether you earn a six-figure income or toil on a low-paying job, this rule can be applied to allocate your finances in the way best suited to your financial situation.

Key Benefits:

- Adaptable budgeting: When you earn more, your dollar amounts increase proportionately, allowing you to save and invest larger sums.

- Adaptable for low-income individuals: If your income is lower, the 50-30-20 Rule provides room to spend more on needs and then allocate the ratios of wants and savings according to your requirements.

- Lifestyle cost flexibility: The rule provides room for flexibility in the event that you stay in a region where the standard of living is costly or your lifestyle costs change from month to month.

Real-Life Applications

Understanding the practice of the 50-30-20 Rule is vital in being able to use it in your own budget. Let’s consider an example of how different portions can utilize this rule depending on their own circumstances:

Young Professional: Dealing with Student Loans and Saving

It can be tough for a young professional to manage saving and student loan payments, even for loans with low interest rates. The following is an example of the 50-30-20 Rule being utilized as a budget example:

- 50% Necessities: Rent, bills, student loan minimum payments, transportation.

- 30% Discretionary: Eating out, entertainment, holiday, and subscription services.

- 20% Savings and Debt Repayment: Emergency fund, extra student loan repayment, retirement savings.

This division allows young professionals to meet current expenses while saving for the future.

Family Budgeting: Family Expenses vs. Children’s Needs

Families can also get the 50-30-20 Rule to work for them by making adjustments to accommodate family expenses, children’s expenses, and savings for the future. Here is a sample budget:

- 50% Needs: Mortgage, utilities, groceries, insurance, childcare.

- 30% Wants: Family vacations, eating out, children’s after-school activities.

- 20% Savings and Debt Repayment: College fund, retirement savings, and debt repayment.

With the application of the 50-30-20 Rule, families can better manage their spending while saving for the future, too.

Retiree Planning: Saving to Last Through Retirement

For retirees, the 50-30-20 Rule helps them from outliving their retirement savings. A general retiree budget could be:

- 50% Needs: Medical care, housing, utilities, insurance.

- 30% Wants: Travel, hobbies, entertainment.

- 20% Savings and Debt Repayment: Paying off debt, investing in health savings accounts (HSAs), and having money reserved for future healthcare expenses.

Retirees can also make use of the 50-30-20 Rule to budget their expenses and ensure their financial security.

Tools and Resources

In attempting to assist you in adhering to the 50-30-20 Rule, we’ve gathered some useful tools and resources:

Interactive Budget Calculator

Interactive Budget Calculator allows you to enter the amount you make each month and get recommended allocations based on the 50-30-20 Rule. If you are beginning the process of budgeting or must make adjustments to your current budget, this calculator gives you the information you require to make improved financial decisions.

Downloadable Budget Templates

Need a quick, printable answer? Employ our 50-30-20 Rule budget forms to make tracking your spending a breeze each month. Our forms break down your income and expenses into categories so that you can easily stay within your means.

Connecting the Rule to Your Lifestyle

The best part about the 50-30-20 Rule is how flexible it can be. Here are a few ways you can adjust the rule to work for you and your unique personal financial situation:

Adjusting Percentages for High-Cost-of-Living Areas

If you live in an area that has a high cost of living (like in a large city), it’s easy to look around and notice that 50% of your income is not enough for all that you need. In this situation, you can adjust the percentages so that you save more for needs. Here’s how:

- 55% Needs

- 25% Wants

- 20% Savings and Debt Repayment

This tweak still keeps you living within your means, but also lets you address your finances.

Tips for Freelancers or Those with Irregular Income

Irregular income earners and freelancers may adjust the 50-30-20 Rule accordingly. The following is how:

- Create a Buffer of Savings

- Save 25-30% in high-income months to create a buffer.

- Use 20 % of the savings allocation in 20% to cover emergencies.

- This buffer will be able to handle low-income months.

- Set up a “Minimum Income” Base

- Calculate your average monthly income for recent months.

- Use it as a basis while budgeting and adjusting 50-30-20 Rule allocation.

- It provides a more secure way of budgeting.

- Save First

- Automate retirement and savings account transfers.

- Save first, even if income is sporadic.

- Saving regularly ensures long-term financial stability.

- Adjust the 50-30-20 Divide

- Divide more to “needs” during times of reduced income.

- Reduce discretionary spending (wants) during times of low income.

- Save 30% or more during times of high income.

- Check and Balance Regularly

- Review your budget at the end of each month.

- Realign the allocations based on actual expenses and revenues.

- Flexibility guarantees that your budget remains current with your finances.

How to Apply the 50-30-20 Budget Rule

Applying the 50-30-20 Budget Principle is simple and hassle-free. It leaves you entirely in control of your money without the hassle of strict spreadsheets or monitoring every last dollar that passes through. Apply the simple steps below to apply it to your daily money routine:

- Calculate Your After-Tax Income

Start by determining your after-tax income and deductions on a monthly basis. That is where you will divide based on the 50-30-20 Rule. If you have a variable income or are self-employed, averaging 3–6 months might be an option.

💡Tip: Count all regular sources of income—salary, side hustles, rent, etc.

- Divide Your Budget in 50-30-20 Percentages

Once you have obtained your after-tax income, do the following based on the rule:- 50% for Needs: Rent/mortgage, groceries/food, transportation, insurance, utilities.

- 30% for Wants: Non-needs that improve the quality of your life—dining out, subscription, hobbies, entertainment.

- 20% for Savings & Debt Repayment: Emergency fund, retirement savings, debt repayment (e.g., loan or credit cards).

- Track and Categorize Your Spending

Go through your past 1–2 months’ spending. Classify each transaction as one of the three types. You’ll get a fair sense of how your current spending stacks up—or doesn’t stack up—to the 50-30-20 Rule.

💡 Tip: Simplify it by following it using a budgeting tool or spreadsheet.

- Maximize Where You Can

If you’re investing 70% in needs or 40% in wants, something gives. Not utopian perfection, but for the best. Take small steps first—cut excessive wasteful wants or spend wisely to save more on needs. - Automate Savings and Set Goals

Transfer the 20% savings compartment to a use. It may be to the emergency fund, credit card payoff, or contribution to a retirement plan—set it to an autopilot mode.

💡 Tip: Schedule an automatic transfer to savings when your paycheck arrives in your account.

- Track Monthly and Adapt

Your budget will be adjusted because life keeps evolving. Check each month’s 50-30-20 proportions to keep up with your financial objectives and adjust whenever necessary

Common Mistakes and How to Avoid Them

Despite the usefulness of the 50-30-20 Rule, everyone commits common mistakes that render the rule moot. The following is a description of such mistakes and how to avoid them:

- Categorizing Wants as Needs

- Mistake: People put discretionary spending, e.g., subscription, eating out, or entertainment, under the “needs” rather than “wants” category.

- Solution: Prioritize needs over wants. Needs are basic necessities for simple survival, such as food, electricity, and shelter, whereas wants constitute discretionary spending that needs to be reduced or eliminated.

- Solution: Prioritize needs over wants. Needs are basic necessities for simple survival, such as food, electricity, and shelter, whereas wants constitute discretionary spending that needs to be reduced or eliminated.

- Mistake: People put discretionary spending, e.g., subscription, eating out, or entertainment, under the “needs” rather than “wants” category.

- Disregard of Savings

- Mistake: Most people spend more than they save, and it has disastrous consequences on total financial health.

- Solution: Always save 20% of your income as debt repayment and savings. Automate the payments to be made on a regular basis, and make savings a required line item on the budget.

- Solution: Always save 20% of your income as debt repayment and savings. Automate the payments to be made on a regular basis, and make savings a required line item on the budget.

- Mistake: Most people spend more than they save, and it has disastrous consequences on total financial health.

- Not Updating the Budget When the Situation Changes

- Mistake: Continuing to spend the same amount of money when your financial situation or salary has undergone a change, i.e., getting a salary hike, moving to a new city, or getting an unexpected bill.

- Solution: Re-check personal budgets and re-apply the 50-30-20 Rule accordingly. Save even more now if your salary has been hiked. Re-calculate budgeting in case of unnecessary expense.

- Solution: Re-check personal budgets and re-apply the 50-30-20 Rule accordingly. Save even more now if your salary has been hiked. Re-calculate budgeting in case of unnecessary expense.

- Mistake: Continuing to spend the same amount of money when your financial situation or salary has undergone a change, i.e., getting a salary hike, moving to a new city, or getting an unexpected bill.

- Not Paying Off Debt

- Fault: Failing to save for the monthly spending or discretionary spending or not saving sufficiently to retire debt.

- Solution: Use some of the 20% savings to pay high-interest debt. Retire debts, particularly credit card debt, as quickly as possible, so money is available to save.

- Solution: Use some of the 20% savings to pay high-interest debt. Retire debts, particularly credit card debt, as quickly as possible, so money is available to save.

- Fault: Failing to save for the monthly spending or discretionary spending or not saving sufficiently to retire debt.

- Budgeting the Budget: Too Complex

- Fault: Budgeting every single last cent, and frustration and burnout result.

- Solution: Keep it simple. Have the major categories (needs, wants, savings) and utilize tools or an app that make expenditure tracking easier to do.

- Solution: Keep it simple. Have the major categories (needs, wants, savings) and utilize tools or an app that make expenditure tracking easier to do.

- Fault: Budgeting every single last cent, and frustration and burnout result.

- Fixed Expense Underestimation

- Error: Not factoring fixed expenses like rent, utilities, or car payments into savings.

- Solution: Always religiously account for fixed expenses. They always eat more of your budget than expected, and having them permits planning.

- Solution: Always religiously account for fixed expenses. They always eat more of your budget than expected, and having them permits planning.

- Error: Not factoring fixed expenses like rent, utilities, or car payments into savings.

- Failure to Save an Emergency Fund

- Mistake: Failing to save an emergency fund or using savings to cover unexpected expenses.

- Solution: Use 50% of the 20% savings pool to build an emergency fund buffer. Having a cushion for the doctor, car repairs, or losing your job will keep money fear at bay.

- Mistake: Failing to save an emergency fund or using savings to cover unexpected expenses.

Pro Tricks to Max Out Your Budget

To maximize the 50-30-20 Rule, add the following pro tricks to get you started:

- Automation Saving

- Tip: Automate savings and investments.

- Why It Works: It removes hands from the portion of your income, and you’re independent with your savings goal.

- Why It Works: It removes hands from the portion of your income, and you’re independent with your savings goal.

- Tip: Automate savings and investments.

- Periodic Checking and Balancing of Your Budget

- Tip: Regularly check your budget and balance accordingly with respect to any change in your revenues or expenses.

- Why It Works: It keeps you flexible, thus your budget is aligned with your today’s life.

- Why It Works: It keeps you flexible, thus your budget is aligned with your today’s life.

- Tip: Regularly check your budget and balance accordingly with respect to any change in your revenues or expenses.

- Setting Short- and Long-Term Financial Goals

- Tip: Establish specific, measurable short-term (vacation savings) and long-term (retirement savings) goals.

- Why It Works: Specific goal statements prevent you from going off track and making more intelligent saving and spending choices.

- Tip: Establish specific, measurable short-term (vacation savings) and long-term (retirement savings) goals.

💡Need to increase your productivity on a budget?

Read our detailed guide on the 1-3-5 Rule for Productivity: Strategies and Examples to stay on target and achieve more every day.

Conclusion: Taking Control of Your Money

50-30-20 Rule is realistic and realistic saving and budgeting. If you are devoting half of your income to necessities, 30% to discretionary spending, and 20% to saving and debt retirement, then you have a balanced budget.

The system enables you to make smart decisions, escape the budget trap, and stay on the path of financial wellness. Regular review and rebudgeting is the key to staying in balance with life’s rollercoaster.

Start now. Budget your money using the 50-30-20 Rule and set yourself on the journey to a financially healthier tomorrow.